Preliminary Results for July 2025

| Jul | Jun | Jul | M-M | Y-Y | |

| 2025 | 2025 | 2024 | Change | Change | |

| Index of Consumer Sentiment | 61.8 | 60.7 | 66.4 | +1.8% | -6.9% |

| Current Economic Conditions | 66.8 | 64.8 | 62.7 | +3.1% | +6.5% |

| Index of Consumer Expectations | 58.6 | 58.1 | 68.8 | +0.9% | -14.8% |

{kind=link}

Read our June 27th special report, June 2025 Update: Current versus Pre-Pandemic Long-Run Inflation Expectations

Next data release: Friday, August 01, 2025 for Final July data at 10am ET

Surveys of Consumers Director Joanne Hsu

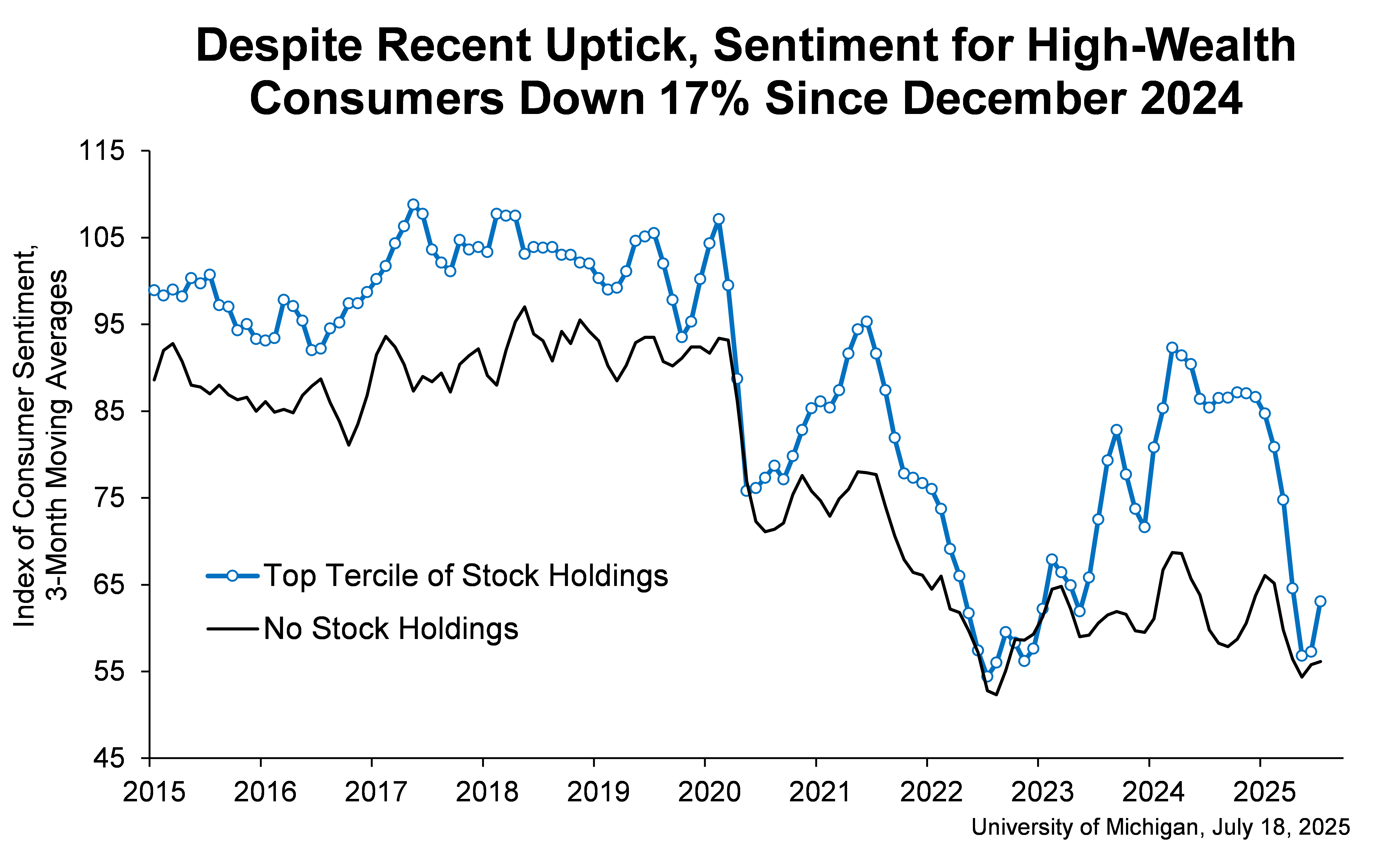

Consumer sentiment was little changed from June, inching up about one index point to 61.8. While sentiment reached its highest value in five months, it remains a substantial 16% below December 2024 and is well below its historical average. Short-run business conditions improved about 8%, whereas expected personal finances fell back about 4%. Consumers are unlikely to regain their confidence in the economy unless they feel assured that inflation is unlikely to worsen, for example if trade policy stabilizes for the foreseeable future. At this time, the interviews reveal little evidence that other policy developments, including the recent passage of the tax and spending bill, moved the needle much on consumer sentiment.

Year-ahead inflation expectations fell for a second straight month, plunging from 5.0% last month to 4.4% this month. Long-run inflation expectations receded for the third consecutive month, falling back from 4.0% in June to 3.6% in July. Both readings are the lowest since February 2025 but remain above December 2024, indicating that consumers still perceive substantial risk that inflation will increase in the future.

Year-ahead inflation expectations fell for a second straight month, plunging from 5.0% last month to 4.4% this month. Long-run inflation expectations receded for the third consecutive month, falling back from 4.0% in June to 3.6% in July. Both readings are the lowest since February 2025 but remain above December 2024, indicating that consumers still perceive substantial risk that inflation will increase in the future.