Preliminary Results for June 2026

| Jun | May | Jun | M-M | Y-Y | |

| 2026 | 2026 | 2025 | Change | Change | |

| Index of Consumer Sentiment | 48.9 | 44.8 | 60.7 | +9.2% | -19.4% |

| Current Economic Conditions | 48.4 | 45.8 | 64.8 | +5.7% | -25.3% |

| Index of Consumer Expectations | 49.3 | 44.1 | 58.1 | +11.8% | -15.1% |

Read our special reports:

5/22/26

National Estimates Continue to Align With Views of Independents5/8/26

Confidence in Financial Institutions1/23/26

January 2026 Update: Current versus Pre-Pandemic Long-Run Inflation Expectations

Next data release: Friday, June 26, 2026 for Final June data at 10am ET

Surveys of Consumers Director Joanne Hsu

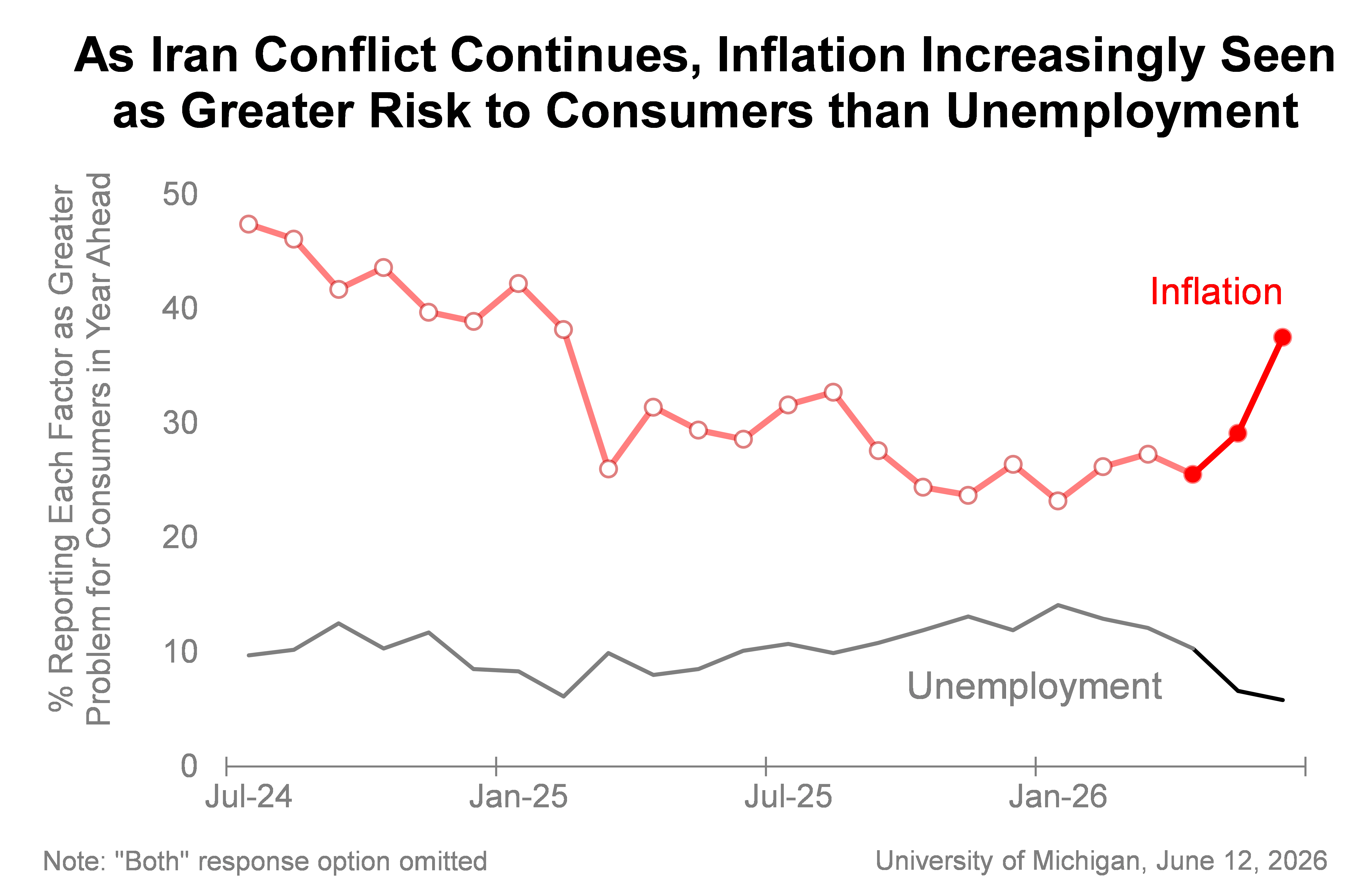

This month, consumer sentiment ticked up about four index points, or 9%, with consumers experiencing some relief due to the early-month easing in gasoline prices. This measured improvement in sentiment was widespread, seen across age, education, and political party. Lower-income consumers exhibited a particularly strong sentiment increase, consistent with the fact that gasoline comprises a larger share of their budgets. Overall, assessments and expectations of personal finances and business conditions all rose this month. Even with June’s early gains, however, views of the economy are still relatively dour. Sentiment is currently 13% below January 2026 and 19% below a year ago, as consumers remain focused on kitchen table issues. They feel burdened by the recent escalation in inflation and worry that higher inflation could remain stubborn going forward, particularly in the short run. Interviews for this release were completed between May 19 and June 8.

Year-ahead inflation expectations inched down from 4.8% in May to a still-elevated 4.6% this month. The current reading substantially exceeds the 3.4% reading seen in February 2026 prior to the start of the Iran conflict, along with all 2024 readings. Long-run inflation expectations fell back from 3.9% last month to 3.4% in June, remaining notably higher than the 2.8% to 3.2% range seen in 2024.

Year-ahead inflation expectations inched down from 4.8% in May to a still-elevated 4.6% this month. The current reading substantially exceeds the 3.4% reading seen in February 2026 prior to the start of the Iran conflict, along with all 2024 readings. Long-run inflation expectations fell back from 3.9% last month to 3.4% in June, remaining notably higher than the 2.8% to 3.2% range seen in 2024.