Preliminary Results for February 2026

| Feb | Jan | Feb | M-M | Y-Y | |

| 2026 | 2026 | 2025 | Change | Change | |

| Index of Consumer Sentiment | 57.3 | 56.4 | 64.7 | +1.6% | -11.4% |

| Current Economic Conditions | 58.3 | 55.4 | 65.7 | +5.2% | -11.3% |

| Index of Consumer Expectations | 56.6 | 57.0 | 64.0 | -0.7% | -11.6% |

Read our special reports:

1/23/26

January 2026 Update: Current versus Pre-Pandemic Long-Run Inflation Expectations11/21/25

National Estimates Continue to Align With Views of Independents

Next data release: Friday, February 20, 2026 for Final February data at 10am ET

Surveys of Consumers Director Joanne Hsu

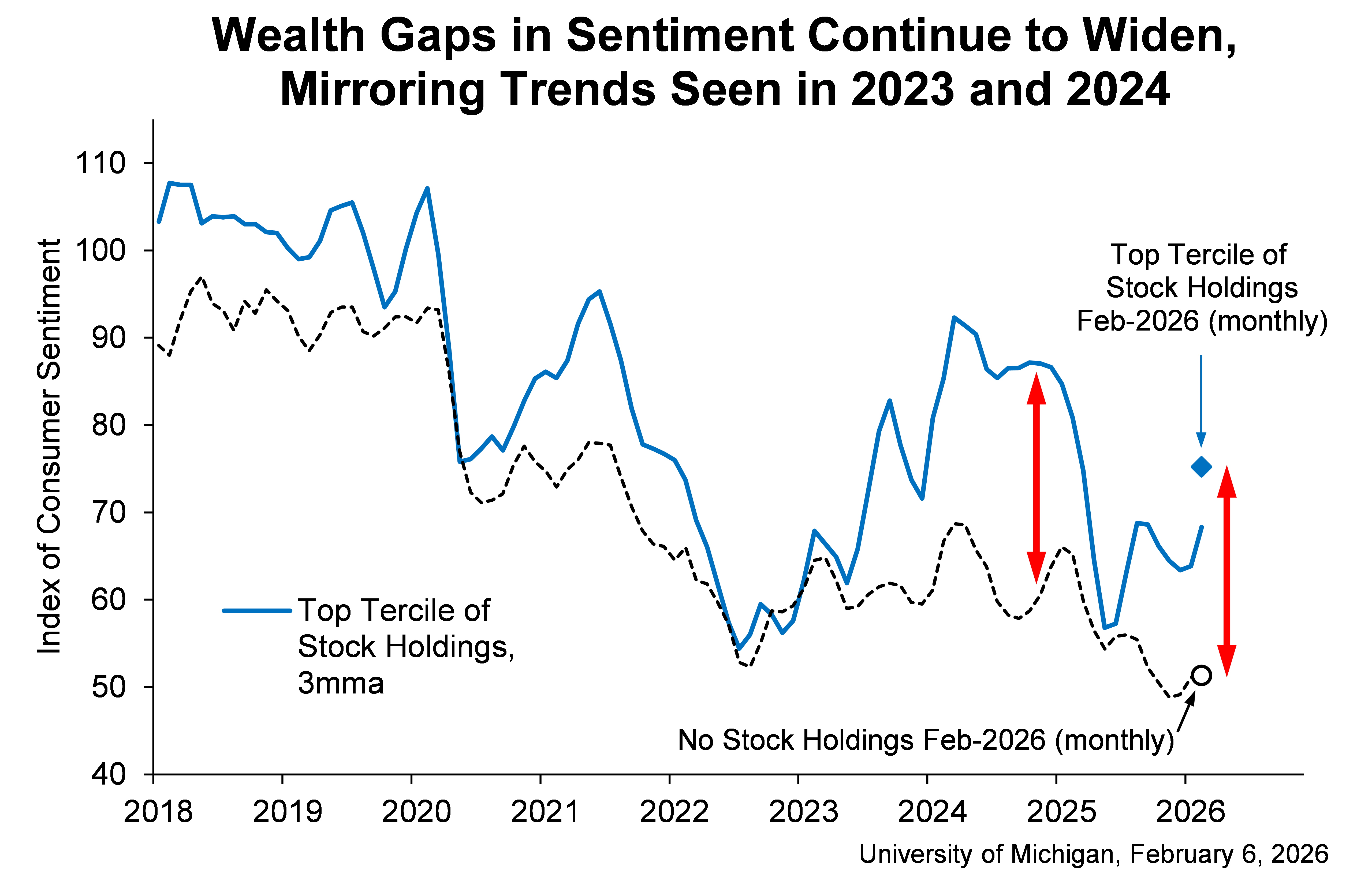

Consumer sentiment was essentially unchanged, inching up less than one index point from last month and sitting about 20% below January 2025. Sentiment surged for consumers with the largest stock portfolios, while it stagnated and remained at dismal levels for consumers without stock holdings. On net, modest increases in current personal finances and buying conditions for durables were offset by a small decline in long-run business conditions. While sentiment is currently the highest since August 2025, recent monthly increases have been small—well under the margin of error—and the overall level of sentiment remains very low from a historical perspective. Concerns about the erosion of personal finances from high prices and elevated risk of job loss continue to be widespread. Interviews for this release cover the two-week period that ended this past Monday.

Year-ahead inflation expectations fell from 4.0% last month to 3.5% this month, the lowest reading since January 2025. This month’s reading still exceeds those seen in 2024 and remains well above the 2.3-3.0% range seen in the two years pre-pandemic. Long-run inflation expectations inched up for the second straight month, from 3.3% last month to 3.4% this month. In comparison, readings ranged between 2.8% and 3.2% in 2024, and were below 2.8% throughout 2019 and 2020.

Year-ahead inflation expectations fell from 4.0% last month to 3.5% this month, the lowest reading since January 2025. This month’s reading still exceeds those seen in 2024 and remains well above the 2.3-3.0% range seen in the two years pre-pandemic. Long-run inflation expectations inched up for the second straight month, from 3.3% last month to 3.4% this month. In comparison, readings ranged between 2.8% and 3.2% in 2024, and were below 2.8% throughout 2019 and 2020.